Traditionally, consulting firms have assisted clients by analyzing problems, needs, and requirements, and delivering a set of documents that clearly detail how to solve the problem, or achieve "gap closure." Although the consultant's work achieved the highest professional and technical standards, many clients could not implement the recommendations and plans due to complexity, lack of resources, or lack of expertise. In response, most consulting firms now perform the gap closure on behalf of their clients, delivering the actual tangible results rather than only providing documented plans and recommendations. This paper provides an overview of this type of consulting service, specifically in a program and project management context serving mergers and acquisitions. The author identifies challenges associated with mergers and integration efforts, and demonstrates how project, program, and portfolio management (PPPM) can offer effective solutions. In addition, the paper provides guidance for selecting the right integration PPPM service provider and engaging the appropriate constituents.

Understanding Contemporary Consulting Services

Traditionally, most consulting firms came to be known as “documents factories.” They would typically engage a client and expend substantial time and resources analyzing their problems, needs, and requirements, and deliver a set of documents that clearly detail how to solve the problem, or, in consulting terms achieve ‘gap closure.’ Though the work of the consultant was typically of the highest professional and technical standards, many clients still found themselves incapable of implementing the recommendations and plans set out in those documents due to complexity, lack of resources, lack of know-how, or for multiple other reasons.

In response, most consulting firms have changed their approaches. They now perform the gap closure on behalf of their clients, meaning that they deliver the actual tangible results rather than documented plans and recommendations. This is the type of consulting service addressed in this paper in a Program and Project Management context serving Mergers and Acquisitions.

Understanding Mergers and Acquisitions

Merger activity commonly originates from the industry. An industry that is experiencing dramatic regulatory reform or rapid technological changes tends to have higher merger activity than one that does not. In some cases, mergers may occur to grant entry to new territories (local or international), expand market share, or to migrate new technologies into the industry. Merger activity is also seen as a solution to increasing competition, especially from international markets. ‘Industry consolidation’ occurs as a means of combining smaller entities into one large company with stronger competitive abilities.

Inherent in their nature, Merger and Acquisition (M&A) activities involve a variety of complexities and risks to the extent that (M&A) agreements typically include provisions for renegotiation or cancellation following events that have a significant negative effect on the company's value or business operations. Although not the prime focus of this paper, it is crucial that on-going projects in target companies are tightly controlled and risk on these projects is adequately managed to avoid adversity that can impact shareholder returns in a typical (M&A) context.

Different Types of Mergers and Acquisitions:

- Acquisition: the purchase of a portion of a target company by an acquirer.

- Merger: the purchase of an entire company, the complete absorption of one company by another.

- Statutory Merger: The target ceases to exist. All assets and liabilities are transferred to the acquirer.

- Subsidiary Merger: The target company becomes a subsidiary of the acquirer, common in cases where the acquired company has a strong brand or good image.

- Consolidation: both companies cease to exist, and a new legal existence is formed.

Classification of Mergers and Acquisitions (Exhibit 1):

Exhibit 1 – Classification of Mergers and Acquisitions

Strategic Directives Motivating Mergers

Any merger stems from a strategic directive identified by the acquirer. Common reasons driving mergers are further listed and explained below. The typical decision-making process starts with research and due diligence leading to a detailed business case that proves that the acquirer would gain benefits they would not be able to realize through organic growth (investment in internal resources and capability). The following strategic directives are not mutually exclusive, meaning that the acquirer may be motivated by one or more of them:

- Creation of Synergies: the new company has greater value than the sum of its parts. Synergies are achieved through creation of economies of scale or aggregation of market share and revenues or a combination of both.

- Growth: Growth in revenue through the investment in external resources (inorganic growth), which is normally faster than organic growth. Also a form of mitigation of risks related to unfamiliarity with new markets, experimentation, and learning curves.

- Increase of Power: When markets are (or close to becoming) saturated, horizontal mergers occur to eliminate or limit competition and expand market share within the non-expandable demographic, thus enabling the influence of prices, and so forth. In its extreme form, this may lead to monopolies. Vertical integration can also considerably reduce competition and increase power through domination of critical supplies or creation of captive markets.

- Acquisition of Unique Capacities and/or Resources: Companies engage in M&As to gain technologies, resources, tools, intellectual property, or other resources that it would either take too long to develop internally or would need to make substantial incentives to achieve, for example, Oracle's acquisition of Primavera in 2009.

- Unlocking Value: Acquirers may identify one or more uncompetitive targets that it believes it can transform into a profitable business through availing resources, organizational restructuring, process reengineering, or other operational enhancements.

- Incentives presented through International Expansion: Common among acquirers seeking to extend their market reach, acquire new manufacturing facilities, develop new sources of raw materials, and access new capital markets, take advantage of lower labor costs, overcome barriers to trade, introduce new technologies to otherwise deprived markets, follow clients as they expand internationally, and/or product differentiation and leverage.

- Diversification: For companies to be seen and managed as a portfolio of investments and to reduce vulnerability to cash flow issues.

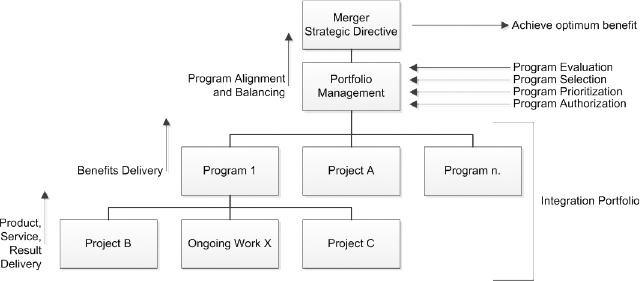

The Integration Portfolio

For the persons involved in the integration, it is important to understand that the Investors and Analysts who architected the merger have thoroughly analyzed and quantified the strategic directives and the rationale behind them to ensure that the merger will create considerable value. The whole purpose of any integration activity would be to maximize the probability that such value would materialize, and manage the realization of anticipated benefits.

Accordingly, any integration effort must be acutely aligned and congruent with such strategic directives and their anticipated benefits. Traditional (business as usual) approaches do not include the governance, tools and techniques, and processes to warrant such alignment. In contrast, Portfolio, Program and Project Management (PPM) do so extensively, as evident through The Standard for Portfolio Management and The Standard for Program Management of the Project Management Institute (PMI). Exhibit 2 below illustrates how PPM aligns and balances programs and projects within the integration portfolio to achieve and realize the optimum benefits anticipated from the merger.

Exhibit 2 – How Formal PPM drives the realization of anticipated benefits

What to expect in a Migration Portfolio

As with any acquisition, the acquirer will want to migrate and integrate its new subsidiary in a manner that best serves its strategic directive and realizes benefits in the shortest timeframe. This will create a portfolio of substantial programs and projects, often cross-cutting multiple domains.

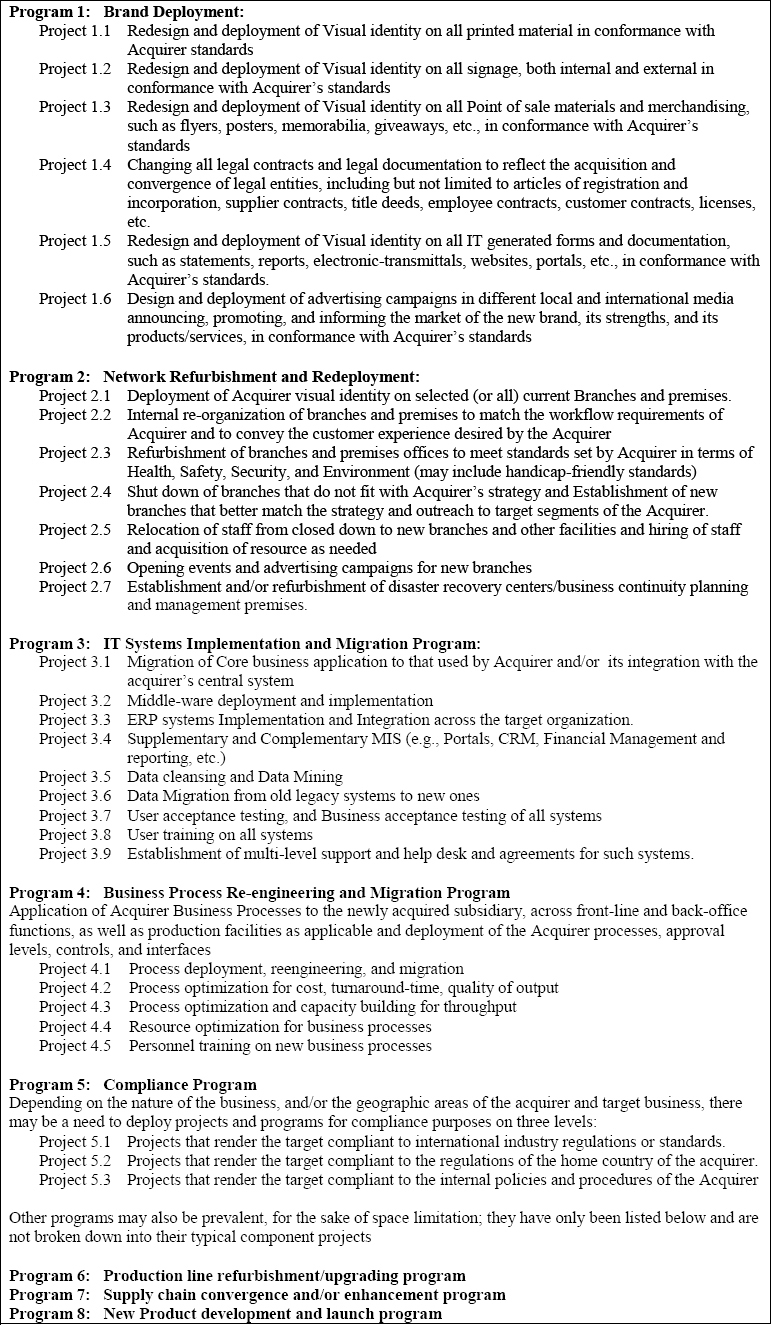

The following is a typical integration portfolio of an Acquirer. Although the portfolio reflects that of one of the author's previous clients, it is generic enough to be considered industry neutral. It is common to witness the programs and projects below in the integration of two banks, two major airlines, or a vertical integration between a mobile phone manufacturer and an electronics distributor. Certainly, not all of the projects and programs listed below apply to all mergers and acquisitions, and there may very well be applicable projects and programs not listed below:

Exhibit 3 – Sample Integration Portfolio

In the actual population of the list above, we have engaged in one of the simplest and first tasks of Portfolio management: Component Identification and Alignment. Typically this would entail the identification, evaluation, selection, and prioritization of programs and projects to serve the purpose of the strategic directive and realize the anticipated benefits.

By examining the above sample portfolio in light of the typical strategic directives, it is evident that delays, over spending, people issues, non-conformance, or risk exposure during the integration process are core reasons why some or all such benefits may not be realized, and why the merger may ultimately fail to meet the strategic directive for which it was originally undertaken.

Undoubtedly, implementing a migration portfolio of such magnitude will present both the Acquirer and the target company with multiple challenges. It would be fair to anticipate that some of the most prominent of these challenges would be as follows:

The Challenges and Solutions through Formal PPPM

Because of space limitations, this section lists only a sample of the total challenges associated with mergers and consequent integration efforts and how PPPM can overcome them.

Challenge #1. The Time factor:

Time is a very important element in any integration, as it has immediate impact on both the smooth operation of the business as well as time to market. Under the merger, the Acquirer will typically want to:

- Capitalize on operational efficiencies by expediting the transition period

- Shorten time to market in order to start realizing anticipated strategic benefit as soon as possible

- Complete the transition in the most comprehensive manner and shortest duration to deliver a strong message to the competition, current customers, and potential customers and expand its market share in doing so.

Most post-acquisition integrations run irreparably behind schedule as a result of the following:

- Addressing the integration portfolio as a series of “Business as usual initiatives,” whereby employees undertake work on these initiatives beside their business as usual tasks, and this eventually leads to significant delays in both, and,

- Not managing such initiatives as structured, rigid, and standard-abiding, governed projects and programs

Such delays inherently lead to:

- Loss of business opportunity — by delaying launches and time to market of new products/services/identities.

- Operational inefficiencies — resources are overwhelmed with additional workloads and cannot perform their regular business-as-usual tasks meet goals or Key Performance Indicators (KPIs)

- Other issues addressed in the challenges below, as they are directly related to time delays.

Solutions to Challenge #1:

Time management is a core area of knowledge in PPPM. At the portfolio level, components (Programs and Projects) are prioritized in order of relevance to the strategic need and benefits realization. Program management involves the development of a high-level program roadmap, program architecture, and a program master schedule. These tools are fundamental to the management of time and regulate the dependencies and interfaces between the program's projects, contributing to either incremental realization of benefits, or integrated realization of benefits at the end of the program, depending on the nature of the program.

At a lower and more detailed level, project management provides the tools and techniques for scheduling and schedule management that allow project managers to explore alternative approaches to achieving project delivery on time, ranging from estimation tools and techniques, to scheduling methods and preferential logic, to scheduling shortening techniques.

For planning purposes, multiple models will be formulated and presented to the management of Acquirer indicating the optimal time frame for the implementation of components and hence benefits in complete alignment with the new strategy. PPM guarantees that only the scheduling approach that best delivers the strategic objectives is used.

The relevance increases when considered in the context of the Strategic Directive. By the application of formal PPPM, stakeholders can clearly see the status of their portfolio, the impact of changes, risks, issues, and dependencies on the portfolio, and how likely the portfolio will achieve anticipated results.

PPM presents tight periodic control of time. This provides Acquirer with guarantees that deliverables will not deviate from plan, and also preempt any such deviation and invoke corrective action as and when needed, with minimum risk and exposure to Acquirer.

Challenge #2. Technical Expertise:

The integration portfolio will require specialized expertise within different domains. While some needed expertise might reside within Target Company and others within the Acquirer, due to the one-off nature of the integration, some will not and will need to be sourced externally.

Any organization seeking to augment its technical expertise for a temporary endeavor such as any one or more of the programs and/or projects listed above will need to adopt administrative processes and burdens that would otherwise not be part of its business as usual. Some of these processes and their consequent implications are:

- Talent acquisition processes: mostly in areas where the organization has no or limited previous experience. This may result in not hiring the best resource for the purpose of the portfolio, and/or extreme delays. Moreover, the organization may simply “not know where to look” for the required talent or not have hiring models (contracts, remuneration models, etc.) that suit the type of engagement and its temporary nature.

- Integration of newly acquired talent: This mainly revolves around having to “blend” the newly acquired resource(s) into the functional structure of the organization, adopting processes, policies, and procedures conventional to the organization, and having to work with existing employees. While this is a normal situation when it comes to ongoing operations, the characteristics of an integration effort render such approach as impractical. Whereas the integration of the new resource(s) may outlive the duration of the integration portfolio, or of the program/project for which the resource(s) was acquired. Ideally, the acquirer would want to hire resources that would “hit the ground running,” and relive themselves from the administrative burden of integrating them into their organization, and any learning curves needed.

- Finally, the acquirer will need to disband such resource(s) when the program or project for which they were acquired is completed. In many markets, cultures, and industries, the concepts of temporary labor are not common, and the labor laws may not accommodate for this type of engagement. At the worst case, the resource(s) may prolong the program/project in favor of keeping the job and the income flowing. In other cases, the governing laws my mandate the acquirer to pay hefty financial compensation to the resource(s) in order to disband them, and in many cases acquirers have simply kept such resources on their head count to avoid legal liability.

Over the years, PPPM Consulting Firms have built a vast network of both local and international experts in most, if not all, of the domains listed above, on both the PPPM and technical levels. As a result, PPPM Consulting Firms are able to:

- Engage such resources with the Acquirer on an as-needed basis to fulfill the objectives of each program/project in a cost effective manner through procurement of the resources/expertise and resource leveling.

- Eliminate any search and recruitment cycles — resources are readily available with succession plans in place.

- All international and local resources are accessible at minimal costs to the Acquirer. Because typically PPPM Consulting Firms call on the services of such experts on multiple portfolios; hence, Firms have developed financial models that are in the best interest of the client.

By accessing hiring such expertise and specialized resources through PPPM Consulting Firms, Acquirer will not need to undertake any of the following:

- Manage such resources

- increase its head-count to meet the need of the projects and programs in the migration portfolio

- Carry the legal and financial burden associated with such resources

- Carry the burden of re-deployment of such resources once their engagement is not needed (projects are delivered).

- Level their allocation across project and program work for operational and financial efficiencies while controlling project duration

- Manage resource scheduling conflicts (which may become very complex on this portfolio)

Challenge #3. Extensive Knowledge of The Local Market:

During its years of operation in any market, the target company undoubtedly accumulates a wealth of knowledge of that market. This knowledge base is usually limited to the core business of the target company — its ‘raison-d’être’— and such knowledge is commonly valued as part of its assets in the merger. The challenge unfolds when faced with an integration portfolio, simply because the target organization and/or acquirer need to do things differently: new scopes of work, shorter delivery times, multiple projects at the same time, multiple contractors at the same time, and other information directly associated with the different program/project domains that would not be needed in the contrasting regular business operations.

As a result of the merger, and to meet the requirements of the strategic directive and realize anticipated benefits, the acquirer will need to temporarily augment its wealth of knowledge with non-conventional means of implementation and delivery to achieve cost, time, quality, and business benefit objectives and efficiencies. Acquiring such market knowledge, while vital, may be very costly, time-consuming, or cumbersome. Moreover, the investment of time and money may not be worthwhile post-integration, adding to the cost of the integration and throwing the business case(s) out of boundaries.

The challenge is magnified in the context of international business, specifically when mergers are conducted across borders or continents.

With their previous in-depth experience in the local markets in which they operate, PPPM Consulting Firms are well poised to provide the Acquirer with the needed knowledge through for the purpose of the integration through their pest practice library. Such skills and knowledge would not be gained otherwise, as they compile rigorous, consolidated lessons learned at the end of each phase of every engagement, identifying what worked well, and what needs improvement. Such firms also follow the ‘Continuous-Improvement Cycle’ to progressively enhance their service delivery.

Formal PPM advocates an integrative approach to managing projects and programs. PPPM Consulting Firms typically integrate PPPM international standards (including but not limited to Project Management Institute's The Standard for Portfolio Management, The Standard for Program Management, and A Guide to the Project Management Body of Knowledge (PMBOK® Guide) with their knowledge of the local market all in the best interest of the Acquirer and with a focus on delivery of anticipated benefits.

An example of such knowledge, for clarification purposes, is that PPPM Consulting Firms have matured models of working with multiple contractors and service providers in cases of integration or ‘aggressive market penetration,’ whereby Firms minimize risk, maximize benefit, expedite time, and optimize cost without compromising on the quality of output. Such knowledge is derived from their previous experiences, and will not be needed as part of business as usual, once the programs have been transitioned into regular operations.

Challenge #4. Budget and Cost Management:

In deploying an integration effort with such magnitude, in light of specific strategic directives and their anticipated benefits, especially if conducted in a market that is new to the Acquirer, the cost of the initiatives may skyrocket. Adding to the adversity, elements such as scope creep, changes, unanticipated risks, lack of capacity and lack of knowledge will certainly cause budget overruns.

Running the integration as a series of Business as Usual initiatives inevitably leads to either underestimating budgets, only to present surprises to stakeholders during their implementation, or the incurrence of various hidden, unanticipated, and sunk costs, or both. Even during the implementation of the most carefully budgeted initiatives, business as usual practices do not employ monitoring and controlling tools and parameters distinct to PPPM such as Earned Value Management, and therefore cannot collectively control cost, time, and scope in relation to one another and provide stakeholders with trend analyses and accurate variance reporting.

Through formal PPPM, Budgets are adequately estimated, using scientific models of scalability and project ‘do-ability’ specific to PPPM. All factors affecting the program/project are integrated into the estimates. Such factors include, but are not limited, risks, dependencies, resource requirements, cost of procurement, cost of quality, etc. For each program and project, multiple models are developed and presented to the management of the Acquirer to ensure benefit/cost trade-offs are optimized and that they are aligned with the business case driving the merger.

During execution, Project and Program Spending is tightly monitored and controlled, using PPPM-specific tools and techniques such as EVM (mentioned above). That will guarantee that cost overruns are kept at a minimum if not eliminated, with all deviations from the budget tightly managed and corrective action implemented as and when needed. Periodic trend analysis helps the Program Management Office highlight to senior management and stakeholders what current project and program performance will lead to in terms of spending.

All changes and variations are also tightly managed, ensuring that their impact is accurately assessed and presented to the management of the Acquirer with sufficient levels of detail, allowing for conscious decision making on whether or not incorporate such change.

Challenge #5. Non-conformance

Conformance is of great relevance to any integration portfolio on three distinct, but often interrelated levels:

1) Regulatory Conformance: The merger will need to comply with the policies and governing laws set out in the merger agreement, the laws of the Acquirer's home country governing mergers, those of the Target organization's country if conducted across borders. Non-conformance can have grave consequences to the viability and sustainability of the business.

2) Conformance to acquirer's standards: Companies that have grown to the size that would enable them to execute an acquisition of another company would have developed governance and quality standards and processes for their practice throughout their evolution. It is only common for acquirers to demand that their target companies apply and comply with such standards.

3) Conformance to quality metrics: Within the integration portfolio, every project will need to comply with the quality metrics identified and agreed for every deliverable.

By conducting the integration to as a series of ‘Business as Usual’ undertakings, companies will overwhelm their resources with complexities related to compliance. The added workload alone will inevitably lead to higher margins of error in the outputs of both work streams, and frustration would arise from the lack adequate tools and techniques to manage quality and conformance.

In one particular case the author experienced first-hand, a merger had been formed between two of the world's largest companies in a very high tech and lucrative industry. Each company came from a different continent, and so their staff members were equally sophisticated, but equally adamant that the standards of their mother company were the best-in-class. This was a multi-billion dollar merger that was on the verge of collapse until PPPM was formally introduced, as with the rest of the challenges, PPPM incorporates the tools and techniques necessary to achieve conformance and avoid risks of non-compliance.

Challenge #6. Stakeholder Management and Communications:

As defined by PMI, stakeholders are all parties that are affected by, or have influence on, the program or project. Stakeholders can be internal to the projects, the Acquiring organization, the target company, or external to all of them. During a merger and consequent integration, the number, type, interests, and degree of influence and power changes in contrast to pre-merger and post-integration times. These changes necessitate the adoption of processes that seek to identify, analyze, and build management and communication plans, engage, and manage stakeholders throughout the merger-integration life cycle, validating relevance and capturing change as the portfolio evolves.

Challenge #7. Risk Management:

As stated in the beginning of this paper, Mergers and Acquisitions involve high levels of risks and uncertainty that can have detrimental impact to their success. Carried on to the migration portfolio, the number of unknowns is higher at the beginning and dwindles towards the end. All standards of PPPM referenced in this paper address risk management and it is common practice for managers of the most elementary level projects to identify and manage risk.

The occurrence of Risk may cause them not to meet any or all of their time, cost, quality, or benefits goals. If this is the case with basic elementary projects, then it is only fair to assume that the impact and probability of risk grows exponentially when a integration portfolio is undertaken due to complexity, magnitude, un-treaded territory for the Acquirer, and other pertinent factors. There will be many unknowns, plenty of dependencies (both internally and externally), multiple stakeholders, and various interfaces, needless to mention the tight deadlines and delivery times.

Globally, many projects have failed because of inadequate risk and issues management, and consequently, the team finds itself in a constant state of fire-fighting when they really should be managing progress and benefits delivery.

PPM mandates that risks are continuously identified, analyzed, and monitored on a project or program, and sound, realistic risk mitigation plans are in place. Senior management is made periodically aware of the risk on the portfolio, mitigation plans, reserve status, and impact. In a formal PPPM environment, all changes to scope, resource availability, time, budget, strategy and configuration are analyzed for risk implications.

Selecting your Integration PPPM Service Provider

As demonstrated above, many Acquirers and/or targets may realize the need but not have access to the necessary PPPM Capabilities in-house. It is important to realize that such capability, at a minimum, should include the following constituents:

- Governance

- Certified Resources

- Processes

- Tools and Techniques

- Methodologies

- Infrastructure

- Program Management Office (PMO) Capabilities

- Best Practice Libraries

Ideally, by becoming their PPPM Partner, the consulting firm transforms itself to become the Program Management Office (PMO) of the acquirer for the purpose of delivering the Integration Portfolio. By doing so the consulting firm immediately provides the acquirer with the necessary infrastructure, tools, human capability, logistical capabilities, controls, governance, manpower, knowledge, and policies and procedures to ensure the realization of anticipated benefits and delivery of component projects in alignment with the strategic directive.

The selected firm's practices should abide by internationally recognized and globally accepted standards of Portfolio, Program, and Project Management. Their team members should have obtained and maintained certification in such standards, as well as demonstrated acts of continuous improvement and extensive experience in complex, diverse projects. Remember that baking a cake is a project, and so is building the Airbus A380.

Another important, often overlooked, characteristic of the ideal firm is that it should be industry-neutral, meaning that its prime area of expertise should by Portfolio, Program, and Project Management as opposed to Oil and Gas or Information Technology or Telecom. Although uncommon, this is a crucial characteristic as the Integration Portfolio will include programs and projects in multiple areas of application. For example, the integration portfolio of American Airlines and U.S. Airlines will include IT Programs, and the Integration portfolio of JP Morgan and Chase Manhattan will include construction Programs. A capable firm should be able to access, deploy, engage, and disengage the needed expertise in the area of application, as opposed to having such expertise overshadow all of its practices, creating significant gaps in other areas. PPPM Expertise and practices would hence become streamlined and focused on the delivery of the benefits anticipated by the acquirer at all times. Some companies choose to directly contract domain-specific service providers; this leaves the client susceptible to the management capabilities of the provider, which are usually biased towards their technical practice.

Just as firms should be Industry-neutral, they should also be supplier-neutral. They must not have any direct relationships with contractors, service providers, and/or suppliers working on any part of the integration portfolio as this is a clear premise for conflict of interest and undermines the service provider's capability to manage the programs and projects in the best interest of the acquirer. As part of their assets, most firms have accumulated extensive databases with lessons learned and evaluative information on most of the prominent local and international suppliers that acquirers will need to contract to deliver the integration portfolio.

The Firm's operational model should adopt legal and procedural mechanisms, which enable them to help the acquirer tender, select suppliers, formulate, agreements and contracts that best serve the purpose of the strategic directive, and provide the needed visibility to monitor performance. The firms should manage delivery on behalf of the acquirer while granting such visibility.

Real-time status and progress reporting should be at the heart of the service level sought. At the onset of the engagement, the Firm should work with the acquirer to establish a Program Communication Management Plan after conducting thorough stakeholder identification and analysis. The outcome of the Communication Management plans should provide the acquirer with both periodic and ad hoc progress, status, and highlight reports at the level of detail desired by the different stakeholders within the organization.

Professional PPM Consulting Firms do not over-promise and under deliver. Their estimates should always be scientifically formulated and derived from experience of the people closest to the work. They should make certain that they set the acquirer's expectations and manage them throughout the engagement in a realistic, trustful, manner.

Chang, R.P., Moore, K.M., Clayman, M.R., Fridson, M.S., & Troughton, G.H. CFA (2012). Corporate Finance: A Practical Approach, Second Edition. Hoboken, NJ: Wiley.

Project Management Institute (2013). A guide to the project management body of knowledge (PMBOK® guide) – Fifth edition. Newtown Square, PA: Author.

Project Management Institute (2008). The Standard for Portfolio Management – Second edition. Newtown Square, PA: Author.

Project Management Institute (2013). The Standard for Program Management – Third edition. Newtown Square, PA: Author.

This material has been reproduced with the permission of the copyright owner. Unauthorized reproduction of this material is strictly prohibited. For permission to reproduce this material, please contact PMI or any listed author.

©2013 Emad E. Aziz, PMP, PgMP

Originally published as a part of 2013 PMI Global Congress Proceedings – New Orleans, Louisiana